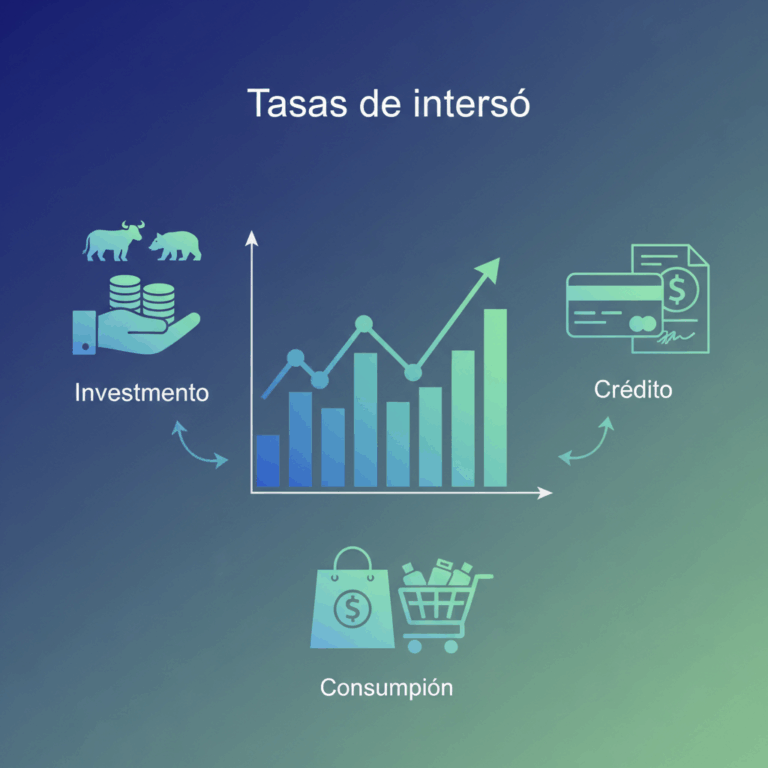

Definition and function of interest rates

The interest rates they represent the price of money over time, being essential to understand the current economy. They function as an indicator of the cost of borrowing money and the profitability of investing it.

This rate affects individuals, companies and governments alike, determining how much is paid for a loan or how much is earned by depositing capital. Its main function is to balance the supply and demand of money in the financial market.

The importance of interest rates lies in the fact that they affect fundamental economic decisions, such as saving, investing or consuming. Its variation directly influences global economic health and day-to-day personal finances.

Concept of interest rates as cost and profitability

The interest rate is the cost assumed by those who borrow money, since you must return the capital plus an additional percentage. It is the consideration for using someone else's capital for a certain time.

For investors, the interest rate is the profitability you obtain by lending or depositing your money. This means that, when investing, they expect to receive a percentage that offsets risk and inflation.

Thus, the interest rate works as a mechanism that balances interests between borrowers and investors, reflecting the supply and demand of funds in the economy.

Importance in economics and personal finances

In the economy, interest rates affect investment, consumption and savings. A change in these rates can accelerate or slow economic growth, as it influences access to credit and financial decision-making.

For personal finances, interest rates determine the profitability of savings and the cost of going into debt. This directly impacts the purchasing power and financing possibilities of families and companies.

Therefore, knowing and understanding interest rates allows us to make more informed decisions and better adapt to changing economic conditions.

Impact of interest rates on investments

The interest rates they decisively influence the behavior of investments, affecting the choice between safe and risky assets. Its variation changes the perception of profitability and risk.

Understanding how rates act on different financial instruments is key to making sound decisions and optimizing the performance of investment portfolios in different economic contexts.

The dynamics between interest rates and markets define economic cycles and determine the confidence and strategies of investors in fixed income, equities and other financial options.

Effect of high rates on fixed income and stock market products

When interest rates rise, the profitability of products fixed income as bonds increase, it often attracts investors looking for security and stable returns.

On the other hand, high rates make business financing more expensive, which can reduce corporate profits and, consequently, negatively affect the market actions.

In this scenario, the stock market may experience lower demand as investors prefer more profitable and less risky fixed income products.

Consequences of low rates on risky investments

In a context of low interest rates, the profitability of safe products decreases, encouraging investors to look for options with greater risk and profit potential.

This situation usually benefits the bag and assets such as investment funds or venture capital, which take center stage for offering better returns compared to traditional fixed income.

However, this behavior can increase the volatility of the market and increase risk exposure of investment portfolios.

Relationship between business financing and interest rates

Interest rates directly influence the cost of financing for companies, affecting their investment and expansion capacity. Low rates facilitate access to cheaper credit.

When financial costs rise, many companies reduce or postpone projects, which can limit their growth while negatively impacting the value of their shares.

Therefore, rate policy affects not only direct investors but also the financial and strategic health of companies in the markets.

Influence of interest rates on credits

The interest rates they are essential to determine the cost of credit accessed by families and companies. Its variation directly impacts the economy and financial behavior of these agents.

An increase in rates makes debt more expensive, which reduces the willingness to borrow. On the other hand, low rates make credit cheaper, promoting access and the capacity for consumption or investment.

Therefore, knowing these effects is key to understanding how financial decisions depend on the economic context and current monetary policy.

Variation in the cost of loans and its impact on families and companies

When interest rates rise, the cost of acquiring a loan increases significantly for families and businesses. This limits borrowing capacity and makes it difficult to finance expenses or investments.

Families can delay major purchases like homes or cars, while businesses face higher costs when financing their operations or expansions.

On the contrary, low rates make loans more affordable, facilitating both family consumption and business investment, driving economic growth.

Effects of rising prices and lower credit prices

The rise in credit prices reduces the demand for loans, which can slow down the economy by reducing spending and investment. In addition, it increases the financial burden for those who already have debt.

On the other hand, lowering credit prices stimulates consumption and investment, facilitating projects and purchases, but it can also encourage excess debt that should be controlled.

Thus, interest rate policy seeks a balance between promoting economic activity and avoiding financial risks derived from excessive credit.

Relationship between interest rates and consumption

The interest rates they are a key factor that directly influences household consumption behavior. Changes in these rates modify the willingness to spend or save.

When rates are low, families tend to take the opportunity to make financed purchases, since the cost of money is more affordable and the incentive to save decreases.

In contrast, high rates often encourage savings and restrict spending, affecting the frequency and volume of consumption in the domestic economy.

Consumption incentives with low rates

With some low interest rates, the cost of obtaining credit is considerably reduced, making it more attractive to finance important purchases such as vehicles, homes or appliances.

Furthermore, the profitability of savings decreases, leading people to prefer to spend rather than save their money, thus increasing overall consumption.

This environment generates a stimulus for the economy, since increased consumption drives production and employment in various sectors.

Preference for savings and reduction of consumption with high rates

When the interest rates are high, the cost of borrowing grows and the attractiveness of savings increases due to better returns on accounts and deposits.

This causes families to prioritize accumulating funds, postponing or reducing expenses, which reduces consumption and can slow down economic activity.

Furthermore, consumer loans become more expensive, discouraging the acquisition of financed goods and especially affecting frequently or highly purchased products.